Plastics machinery shipments drop in Q1 of 2026

Shipments of primary plastics machinery in North America in the first quarter of 2026 dropped from the previous quarter, but increased year over year (YoY), according to the Plastics Industry Association’s Committee on Equipment Statistics (CES).

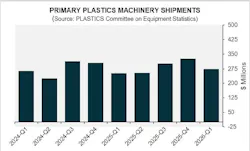

The total shipment value for Q1 was estimated at $273.5 million, down 16.4 percent quarter over quarter (QoQ) but up 8.5 percent YoY.

Twin-screw extruder shipments fell 51.2 percent QoQ and 52.7 percent YoY, and single-screw extruders decreased 24.4 percent QoQ and 26.2 percent YoY.

Injection molding shipments declined 13 percent QoQ, but rose 19 percent YoY.

“First-quarter shipments are usually lower than fourth-quarter shipments, as business momentum tends to slow following a typically busy final quarter of the previous year,” said Perc Pineda, chief economist at the Plastics Industry Association (PLASTICS).

Despite higher tariffs, shipments increased in the second half of 2025. Previous market adjustments across the plastics industry supply chain amid the tariffs likely came at a cost to businesses, many of which were unable to pass on higher costs to customers because of existing contracts, the association said in a news release.

“At the turn of 2026, businesses likely adjusted their pricing contracts to reflect higher tariff costs, which is a second reason why plastics equipment shipments reversed by double digits,” Pineda said.

The customs value of plastics machinery imports totaled $930.4 million in the first quarter, down 1.8 percent YoY. But calculated duties more than tripled, increasing from $39 million in the first quarter of 2025 to $118.9 million in the first quarter of 2026.

Survey respondents’ optimism about market conditions also declined. The share anticipating deterioration in the next quarter increased from 13 percent to 20 percent, while the share expecting conditions to improve over the next 12 months fell from 39 percent to 29 percent.

The U.S. economy expanded by 2 percent in the first quarter, while PLASTICS’ monthly plastics demand estimate averaged $22.7 billion over the last 12 months as of February.

In a separate economic assessment posted May 12 on PLASTICS’ blog, Pineda said plastics product manufacturing improved slightly month over month, rising 0.7 percent from February to March, and plastics production has increased over the last five months, but the overall manufacturing market remains soft.

“It is difficult to ascertain whether the recent monthly increases are the beginning of a sustained rise in plastics product manufacturing,” Pineda wrote.

He noted the U.S. Institute for Supply Management’s Manufacturing PMI was in expansion territory at 52.7 percent in March, the third consecutive month above the growth threshold of 50, and that long-term data on plastics production shows manufacturing hovering around 2017 levels.

Pineda cited interest rates and tariffs as factors holding back production.

“Plastic products manufacturing is sensitive to short-term interest rates both directly and indirectly. Major capital expenditures in plastics manufacturing — such as equipment — rise and fall with borrowing costs. Major end markets of the plastics industry, such as construction, motor vehicles and light trucks, are also interest-rate-sensitive. Thus, plastics production reacts to changes in monetary policy through both direct and indirect channels,” he wrote.

Production trended down from late 2023 through 2024, then “what appeared to be a reversal in the downward trend in plastics production was cut short as trade and tariff policy conditions shifted,” he wrote.

The increased tariffs have had an uneven effect on the plastics industry, weighing on the cost of imports, and cannot single-handedly revive domestic production; regulatory relief, tax incentives and policies supporting workforce supply and development are also needed, Pineda wrote.

“While recent indicators might suggest stabilization in manufacturing activity and a gradual improvement in the plastics industry, the recovery remains uneven, below its long-term trend, and sensitive to changing financial conditions. Given continued pressure on capital investment and interest-rate-sensitive end markets, interest rates may need to come down further to support a more durable and broad-based recovery in manufacturing and plastics production ,” he wrote. “The plastics industry remains resilient, but the pace and durability of recovery will depend on monetary policy, manufacturing activity and broader economic conditions in the months ahead. These broader conditions, against the backdrop of evolving tariff policy and ongoing geopolitical conflict, will also influence the outlook for the plastics industry.”

About the Author

Lynne Sherwin

Managing Editor

Managing editor Lynne Sherwin handles day-to-day operations and coordinates production of Plastics Machinery & Manufacturing’s print magazine, website and social media presence, as well as Plastics Recycling and The Journal of Blow Molding. She also writes features, including the annual machinery buying survey. She has more than 30 years of experience in daily and magazine journalism.